Where is NOL reported?

If you carry forward your NOL to a tax year after the NOL year, list your NOL deduction as a negative figure on the “Other income” line of Schedule 1 (Form 1040) or Form 1040NR (line 8 for 2020). 1040 Instructions: Include on line 8 any NOL deduction from an earlier year.

What is the carryforward period for an NOL generated in 2019?

five years

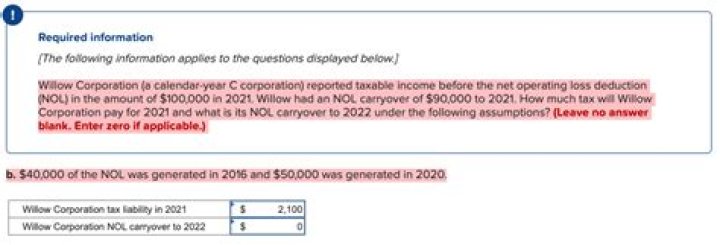

Under the TCJA rules, businesses couldn’t carry back NOLs. Under the CARES Act, an NOL from a tax year beginning in 2018, 2019 or 2020 can be carried back five years.

Can an individual have a NOL?

You may have an NOL if a negative amount appears in these cases. Individuals—You subtract your standard deduction or itemized deductions from your adjusted gross income (AGI). Estates and trusts—You combine taxable income, charitable deductions, income distribution deduction, and exemption amounts from your Form 1041.

Is the net operating loss included in the NOL?

Certain types of losses and deductions are generally excluded from the NOL calculation, including: Most net operating losses are related to business losses. To take the loss, you must include it on your personal tax return.

What are the rules for using a Nol?

The basic rules for using an NOL are: Carry the amount back to the preceding two tax years and apply it against any taxable income, which can generate an immediate tax rebate.

Why was the NOL carryback period changed in 2009?

At the height of the mortgage crisis, in order to stimulate the economy, the American Recovery and Reinvestment Act of 2009 increased the NOL carryback period from two years to up to five years for tax years beginning or ending in 2008. The goal was to allow taxpayers to quickly carry back losses to profitable years and receive tax refunds.

How does the presence of NOLS affect the price paid by an acquirer?

Despite this restriction, the presence of a large NOL can impact the price paid by an acquirer to the shareholders of an acquiree, since it impacts the net-of-tax cash flows that an acquirer will derive from the ongoing results of an acquiree. Section 382 can create a significant problem when a business has large unused NOLs on its books.