Where does a loss go on the income statement?

Just because you haven’t realized a loss yet doesn’t mean you can ignore it in your financial statements. You report unrealized losses and gains on the balance sheet as “other comprehensive income.” The balance sheet includes three sections: owners’ equity, liabilities and assets.

How do you calculate loss on income statement?

To calculate the accounting profit or loss you will:

- add up all your income for the month.

- add up all your expenses for the month.

- calculate the difference by subtracting total expenses away from total income.

- and the result is your profit or loss.

Do losses go on income statement?

Losses are similar to gains in that both are recognized on the income statement only when an asset is sold and a loss is taken. Like gains, there can also be unrealized losses.

What are losses in an income statement?

Losses result from the sale of an asset (other than inventory) for less than the amount shown on the company’s books. Since the loss is outside of the main activity of a business, it is reported as a nonoperating or other loss. To learn more, see Explanation of Income Statement.

How do you account loss?

Accounting for Material Losses Material losses are accounted for in much the same manner as expenses on the accounting ledger. The loss is recorded as a debit on the ledger’s left side and then a corresponding credit is recorded on the ledger’s right side.

What are the types of losses?

Types of Losses

- Immigration. These losses are usually profound, involving as they do so many of life’s anchors and stabilisers.

- Physical Losses.

- Relationship Losses.

- Psychological Losses.

- Sundry Losses.

- Losses of Freedom.

- Losses Resulting from Significant Trauma.

Where is loss on sale of asset on a income statement?

A loss in disposal of plant asset is shown in income statement as an expense (Subtracted from our profit). The asset is written off from the balance sheet.

Where does loss appear in balance sheet?

Net accumulated Loss is shown on the asset side in the balance sheet.

How do you show net loss on an income statement?

A net loss appears on the company’s bottom line or income statement. Net profit or net loss is calculated using the following formula: Revenues – Expenses = Net Profit or Net Loss.

What is the difference between balance sheet and income statement?

Timing: The balance sheet shows what a company owns (assets) and owes (liabilities) at a specific moment in time, while the income statement shows total revenues and expenses for a period of time. The income statement is used to evaluate performance and to see if there are any financial issues that need correcting.

How do you show expenses on a balance sheet?

In short, expenses appear directly in the income statement and indirectly in the balance sheet. It is useful to always read both the income statement and the balance sheet of a company, so that the full effect of an expense can be seen.

Why is the income statement called the profit and loss report?

This is why the Income Statement is also called the Profit and Loss Report! Below we show our Chart of Accounts and our Balance Sheet. The accounts that are reported on the Balance Sheet are shaded: assets, liabilities, and equity. Recall the accounting equation we learned above: Assets = Liabilities + Owner’s Equity.

How are asset disposals reported on the balance sheet?

Balance Sheet The balance sheet is one of the three fundamental financial statements. These statements are key to both financial modeling and accounting by removing a capital asset. Also, if a company disposes of assets by selling with gain or loss, the gain and loss should be reported on the income statement.

Where do gains and losses go on an income statement?

Gains and losses from asset sales then go below operating profit on the income statement. They might appear on their own line, or they could get lumped in with other things in a catch-all category such as “other income” or “nonoperating income.”

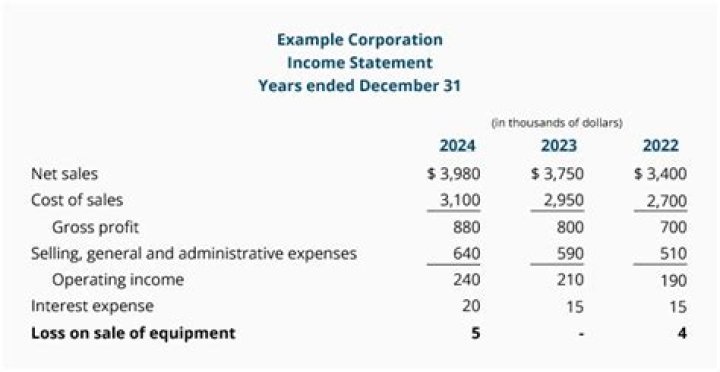

Where is a loss on disposal of a plant asset reported in?

Show the loss of $10m as an expense in profit or loss statement. A loss in disposal of plant asset is shown in income statement as an expense (Subtracted from our profit). The asset is written off from the balance sheet. Cash received is shown as an asset in balance sheet.