What is the penalty for not filing form 5471?

Failure to timely file a Form 5471 or Form 8865 is generally subject to a $10,000 penalty per information return, plus an additional $10,000 for each month the failure continues, beginning 90 days after the IRS notifies the taxpayer of the failure, up to a maximum of $60,000 per return.

Can I amend 5471?

According to the Form 547 1 instructions, a person who previously filed an Form 547 1 but mistakenly provided incomplete or inaccurate information on the form can file an amended Form 547 1 .

Did not file Form 5471?

Fines and penalties for not filing Form 5471 If you meet the requirements and don’t file, you may be hit with a $10,000 penalty for each annual accounting period of the foreign corporation. If you get a notice from the IRS and you don’t file within 90 days, you could have to pay a maximum of $60,000.

When to file Form 5471 for a foreign corporation?

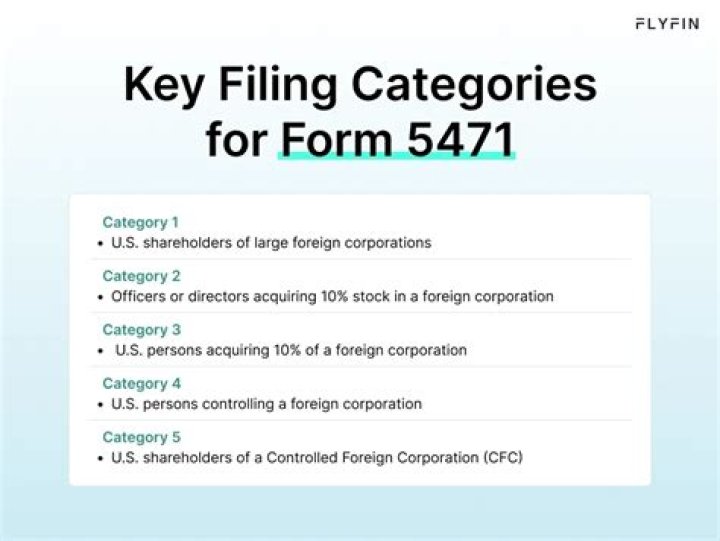

FILING IRS FORM 5471 FOR A FOREIGN CORPORATION. If you as a US Citizen own 10% or more of a foreign corporation (a corporation organized outside of the USA) you are obligated to filed Form 5471 each year with your personal tax return (or your business corporation or LLC tax return if that is the owner of the foreign corporation).

Is there a penalty for not filing Form 5471?

So, there is some work required in converting financial statements to the required format. If you own part or all of a foreign corporation, and have not done your form 5471 filing, you should start filing it immediately to avoid the $10,000 penalty.

When do you have to pay 5471 tax on profits?

This is to the extent that the earnings exceed a 10% return on tangible assets allocated to the U.S. shareholder. It is probable if there is a profit, you will have to pay 5471 tax on the profits. To learn more, check out our article on Form 8992 and the GILTI Calculation.

Where do I enter Pas code on Form 5471?

A Schedule I-1 that includes passive category income must include the code for passive category income (PAS) in the entry space for separate category (at the top of Schedule I-1). A taxpayer with only general category income (and no passive category income) should enter the code “GEN” in the entry space for separate category.