What happens if you fail to file form 709?

If you fail to file the gift tax return, you’ll be assessed a gift tax penalty of 5 percent per month of the tax due, up to a limit of 25 percent. If your filing is more than 60 days late (including an extension), you’ll face a minimum additional tax of at least $205 or 100 percent of the tax due, whichever is less.

Does the IRS audit gift tax returns?

If the value is understated by 25% or more, the IRS has six years to make a challenge. Without a gift tax return, there is no statute of limitations. The IRS can challenge the value of gifts after your death and force your heirs to defend them. In an estate audit, the IRS can look back at all lifetime gifts.

What do I need to report on Form 709?

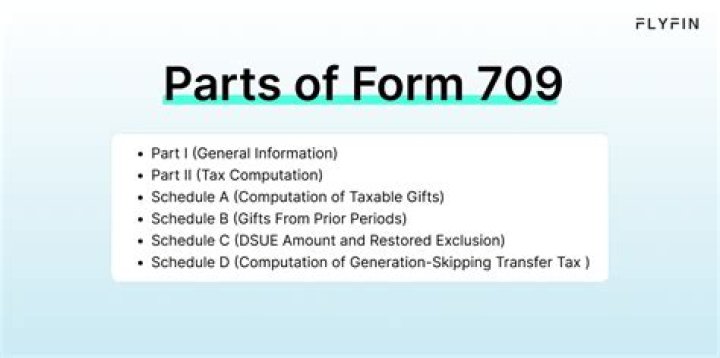

Report the gifts on Schedule A: Computation of Taxable Gifts. Here, you’d provide information such as a description of the gift, the recipient, and its value at the time it was made. You may also report transfers subject to the gift tax and/or generation-skipping transfer tax if applicable. In addition, you’d report transfers made to trusts if any.

Do you have to file a 709 gift tax return?

Officially, it’s called the United States Gift (and Generation-Skipping Transfer) Tax Return. If you make a joint gift with your spouse, each individual must fill out a Form 709. There is no joint Form 709. However, you won’t need to pay an actual tax unless you go beyond your lifetime gift and estate tax exemption.

Where do I find the unified credit on Form 709?

It is located on the first page of Form 709. Refer to the “Table for Computing Gift Tax” under instructions to calculate the tax on the amount of reported gift or gifts. You may apply your lifetime gift and estate tax exemption, also known as the unified credit. So you don’t have to pay an out-of-pocket tax if you use this exemption.

Where does the restored exclusion amount go on Form 709?

The Restored Exclusion Amount will have to be accounted for the donor on every subsequent Form 709 (and Form 706) that will be filed. This means that on all future Forms 709 that will be filed, the Restored Exclusion Amount will need to be entered on Schedule C.