What gets reported on a W-2?

The IRS requires employers to report wage and salary information for employees on Form W-2. Your W-2 also reports the amount of federal, state and other taxes withheld from your paycheck. As an employee, the information on your W-2 is extremely important when preparing your tax return.

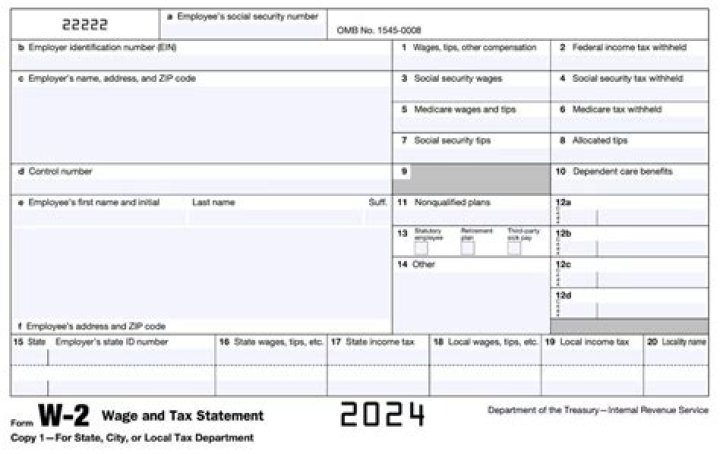

What is reported in Box 12 of W2?

The W-2 box 12 codes are: A — Uncollected Social Security or RRTA tax on tips. Include this tax on Form 1040 Schedule 2, line 8, check box c and, in the space next to that box, enter the amount of the tax and the code that identifies it, here as “UT”. B — Uncollected Medicare tax on tips.

What is reported in box 12a on W-2?

The W-2 box 12 codes are: A — Uncollected Social Security or RRTA tax on tips. Include this tax on Form 1040 Schedule 2, line 8, check box c and identify as “UT”. C — Taxable costs of group-term life insurance over $50,000 (included in W-2 boxes 1,3 (up to Social Security wages base), and box 5).

How is the value of room and board calculated?

The value of the benefit is calculated by the employer and included as income on the employee’s W-2 form at the end of the year. The IRS considers this type of arrangement as just another way to pay employees without giving them cash.

When is room and board considered a taxable benefit?

Taxable Room and Board If an employer offers room and board to an employee and it does not meet the above criteria, it will be considered a taxable fringe benefit and part of the employee’s income. The value of the benefit is calculated by the employer and included as income on the employee’s W-2 form at the end of the year.

Where does the cost of housing go on a W-2?

You will need to include this value on the employee’s annual W-2 form in Box 1, along with other fringe benefits. Use the fair market value of the cost to determine the amount. Any amounts the employee pays for rent or the housing cost are deducted from the W-2 amount.

Can a employer exclude the value of lodging from gross income?

In general, and as stated above, for an employee to exclude from gross income the value of lodging provided by the employer, the employer must require the employee to accept the lodging on the employer’s business premises as a condition of employment. Some educational institutions furnish lodging to their employees.