How are special trusts taxed?

Special trusts are taxed at a sliding scale from 18% to 45% (same as natural persons). Top Tip: In order to claim the benefits applicable to a Special Trust Type A (for example relief from Capital Gains Tax under certain circumstances), the trustees should apply at a SARS branch for classification.

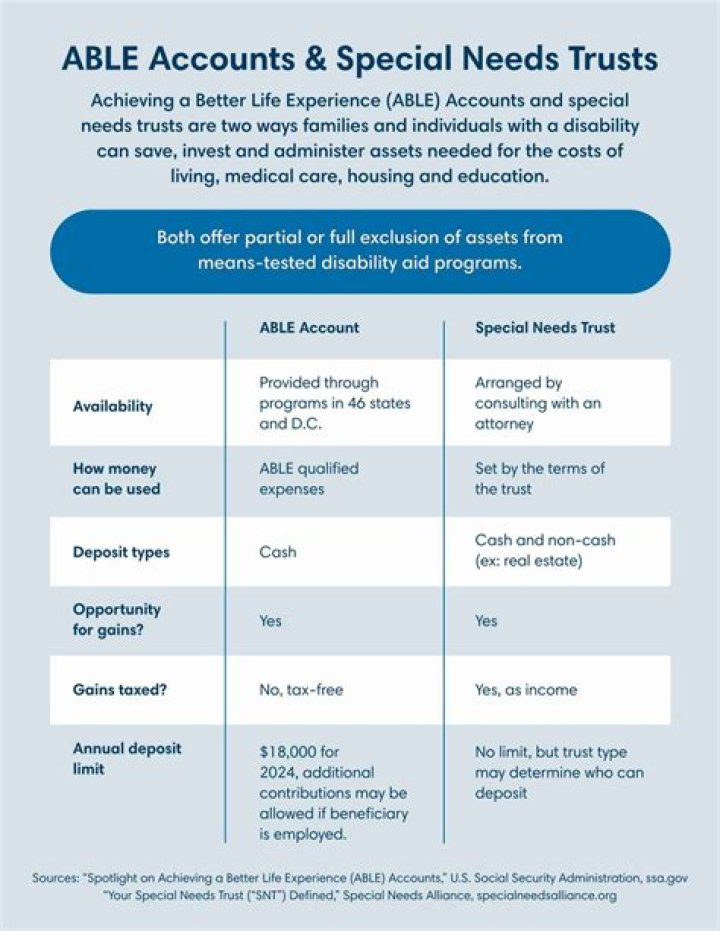

What is the best way to fund a special needs trust?

Ultimately, there are a number of strategies parents and families should consider:

- Insurance – Consider various scenarios in order to sort through the many options. Second-to-die, or survivorship, life insurance policies can be a cost-effective SNT funding choice.

- Real Estate.

- Retirement Plans.

How is a special needs trust taxed?

First Party Special Needs Trusts generally always receive the tax classification of a “grantor trust.” This tax classification means that all of the items of income, deduction, and credit generated by the trust should be reflected on the personal income tax return of the individual with the disability, who is the trust beneficiary.

When to file a 1099 for a special needs trust?

Some trustees obtain a separate taxpayer identification number (TIN) for the first-party SNT when it is established. As a result, when financial institutions report how much income the SNT has earned, a Form 1099 will be issued to the trustee reflecting the SNT’s separate TIN.

What is a first party special needs trust?

First party special needs trusts are funded with the assets of an individual with a disability who is typically participating in a means-tested government benefit program such as Supplemental Security Income or Medicaid. First Party Special Needs Trusts generally always receive the tax classification of a “grantor trust.”

What kind of tax return do I need for a trust?

Form 1041 is the U.S. Income Tax Return for Estates and Trusts. Similar to a Form 1040 on which individuals report their income annually to the federal government, Form 1041 is the form on which most trustees and other fiduciaries (i.e., executors, personal representatives and administrators of estates) report income to the federal government.