Do I have to pay taxes on equity from refinance cash-out?

A cash-out refinance loan essentially turns some of the home equity you’ve built up into cash. It does this by refinancing your remaining mortgage balance to a new, larger loan and giving you the difference. You do not have to pay income taxes on the money you get through a cash-out refinance.

Can you write off HELOC interest?

Interest on a HELOC or a home equity loan is deductible if you use the funds for renovations to your home—the phrase is “buy, build, or substantially improve.” To be deductible, the money must be spent on the property whose equity is the source of the loan.

Can you refinance a HELOC to a home equity loan?

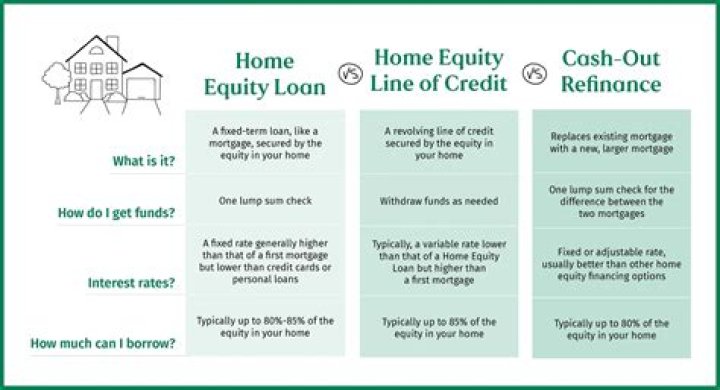

You may be able to refinance the HELOC itself, either to another HELOC or to a home equity loan with a fixed interest rate and payment. Both these typically have the advantage of lower closing …

Is the interest paid on a HELOC tax deductible?

(See Home Equity Loan vs. HELOC .) Interest paid on either loan, like the interest on your first mortgage, is sometimes tax-deductible. Since the Dec. 2017 tax law changes, whether interest on any kind of HELOC or home equity loan is tax deductible depends on how you are spending the loan funds.

How long does it take to pay off a HELOC loan?

There are many forms of HELOC with varying terms — 15 years is a popular one. The loan will have a “draw” phase, followed by a “repayment” phase. During that first phase, which might last 10 years, you can borrow as much as you want up to your limit, pay back sums you choose and then reborrow back up to that limit.

What are the tax implications of a cash out refinancing?

Tax rules for cash-out refinancing. Instead, funds obtained through a cash-out refinance and used for purposes other than home repairs and improvement are considered a home equity loan for tax purposes. Interest paid on home equity loans is still tax-deductible, but only up to a maximum of $100,000 in debt for a couple,…