Can you take out a loan to exercise stock options?

While loans are an option for getting the cash you need to exercise your stock options, they carry a lot of personal risk. And they might not be enough to cover the entire exercise cost to begin with. Rather than a loan, you can also take non-recourse financing.

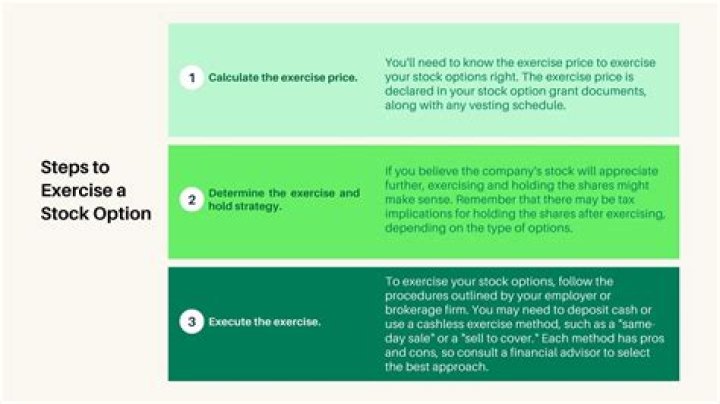

How do you exercise stock options?

Exercise your stock options to buy shares of your company stock, then sell just enough of the company shares (at the same time) to cover the stock option cost, taxes, and brokerage commissions and fees. The proceeds you receive from an exercise-and-sell-to-cover transaction will be shares of stock.

What is non-recourse loan means?

A non-recourse loan is one where, in the case of default, a lender can seize the loan collateral. However, in contrast to a recourse loan, the lender cannot go after the borrower’s other assets—even if the market value of the collateral is less than the outstanding debt.

Can I use stock options to qualify for a mortgage?

Mortgage lenders have specific guidelines for would-be homeowners who want to use restricted stock income toward their mortgages. Vested restricted stock units and stock options usually cannot be used for reserves if they are being used for qualifying income.

Can you borrow to buy options?

While loans are an option for getting the cash you need to exercise your stock options, they carry a lot of personal risk. Rather than a loan, you can also take non-recourse financing. It looks a lot like a loan, but it’s different: with non-recourse financing, your personal assets are not on the line.

Do stock options count as income for mortgage?

Once RSUs vest, they are considered income. Typically an employer will withhold some of the shares to pay taxes on that income. While an RSU may sometimes be considered as qualifying income, stock options will never be considered income by a mortgage lender.

Can you use bonus income to qualify for a mortgage?

If your compensation plan includes bonuses, you may be able to use this as an additional source of income when qualifying for a home loan. Similar to overtime income, in order to be considered for qualifying, lenders want to see a regular history of bonuses being received over a period of two years or more.

Can options make you owe money?

On Puts you lose your cash collateral. If a “buy” or “long” option expires “in the money,” your broker will exercise it, and you will be responsible for buying 100 shares of the underlying stock for each option. So yes, you could owe money on the options.

What is a non-recourse promissory note?

A non-recourse promissory note is a note that prohibits the lender from attempting further restitution from the borrower in case of default. Non-recourse promissory notes are often used for securing a mortgage loan.

What is a repurchase option?

Updated July 14, 2020: A repurchase option is a term used when a company originally issues stock shares. It allows the company to repurchase the shares from the shareholders who own them at a later date. A repurchase option may be used for a number of reasons by a company.

How to find a non recourse commercial loan?

To understand more about non-recourse loan options, contact one of our commercial mortgage lenders by calling 866-647-1650 or using the Contact Us form available from the menu. We’re always happy to work with investors to find the right non-recourse commercial loan rates and repayment plans to suit your needs.

Can a personal guarantee be triggered in a non recourse loan?

In a non-recourse commercial loan: the non-recourse lender would have no such remedy. Exception: Even with a non-recourse loan there may be instances where a personal guarantee could be triggered – commonly referred to as recourse carve-outs or bad-boy carve-outs.

Which is the best non recourse real estate funder?

Investment in real estate is most successful when it’s built on strong relationships and we have them. So put your trust in Clopton Capital to locate the best non-recourse property funders.

How much money is owed to a with recourse loan?

A lender is owed $2 million at the time of a property foreclosure. After retrieving the property, the lender sells it for only $1.5 million incurring a $500k deficit on the advance to the borrower. In a with recourse loan: the lender can look to the “with recourse” borrower to make up the difference based on its/his/her personal guarantee.