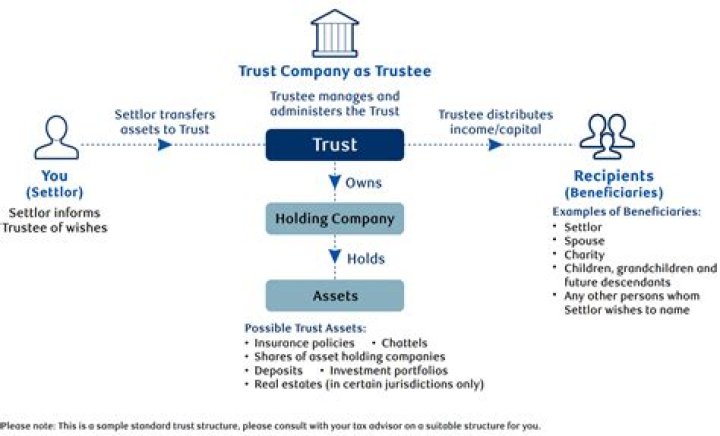

Can US trust have foreign trustee?

Since “all” substantial decisions must be made by a US person, choosing a non-US family member (i.e., a non-US citizen or foreign national who is a non-US resident) as trustee will mean the trust will fail the control test. As such, the trust will be treated as a “foreign” trust.

What qualifies as a foreign trust?

The Internal Revenue Code unhelpfully provides that a foreign trust is any trust that is not a domestic trust. Accordingly, whether a trust is a foreign trust is determined by analyzing whether the trust does or does not qualify as a domestic trust for U.S. federal tax purposes.

Who is an owner of a foreign trust?

IRC section 679 applies specifically in the context of foreign trusts and will treat as an owner of a foreign trust a U.S. person who transfers assets to a foreign trust which has or is presumed to have a U.S. beneficiary.

Do you have to report income from a foreign trust?

Foreign grantor trusts: 1. U.S. grantor (U.S. citizen or resident): During his or her lifetime, the U.S. grantor must report all items of trust income and gain on his or her Form 1040, U.S. Individual Income Tax Return, for the year earned. The trust itself will not be subject to U.S. income tax.

What are the tax consequences of a foreign trust?

Tax consequences can apply to U.S. persons who are treated as owners of a foreign trust and U.S. persons treated as beneficiaries of a foreign trust, and to the foreign trust itself. There can be income tax as well as transfer tax consequences that should be considered.

When does a hybrid trust become a foreign trust?

Under the IRS Code a trust is automatically a foreign trust when a controlling person is not subject to US court supervision and/or the trust is not fully controlled by US persons. The advantage of the Hybrid Trust is that there could be no direct reporting to the IRS even if the financial assets of the trust fund are managed within the US.